Weekly Economic Calendar: Week of February 16 - 21, 2026 (GMT+8)

This week’s macro calendar is driven by the FOMC Meeting Minutes (Thu 03:00) as the main USD volatility anchor (UTC+8). Mid-week, RBNZ Interest Rate Decision (Wed 09:00) is the key NZD risk event, while UK CPI (YoY) (Wed 15:00) and U.S. Durable Goods Orders (Wed 21:00) can add meaningful inflation and growth-driven swings. Later in the week, U.S. Initial Jobless Claims (Thu 21:30) and the U.S. Philadelphia Fed Manufacturing Index (Thu 21:30) shape near-term rates and activity expectations.

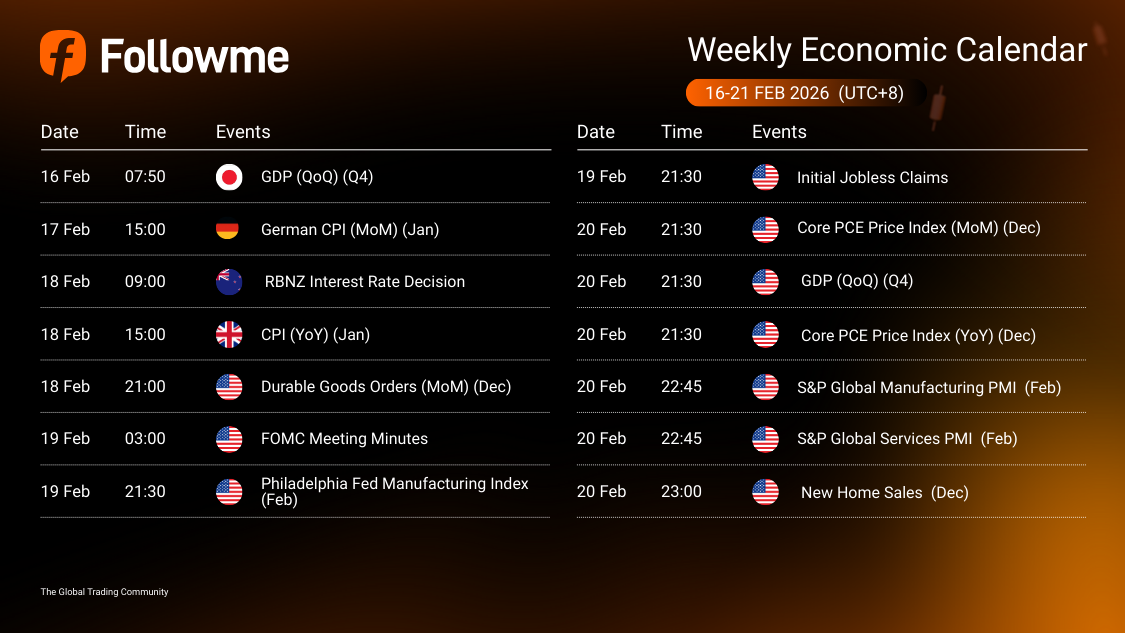

| Time | Cur. | Events | Fcst | Prev |

| JPY | GDP (QoQ) (Q4) | |||

| EUR | German CPI (MoM) (Jan) | |||

| RBNZ Interest Rate Decision | ||||

| CPI (YoY) (Jan) | ||||

| Durable Goods Orders (MoM) (Dec) | ||||

| Philadelphia Fed Manufacturing Index (Feb) | ||||

| Initial Jobless Claims | ||||

| Core PCE Price Index (MoM) (Dec) | ||||

| GDP (QoQ) (Q4) | ||||

| Core PCE Price Index (YoY) (Dec) | ||||

| S&P Global Manufacturing PMI (Feb) | ||||

| S&P Global Services PMI (Feb) | ||||

| New Home Sales (Dec) |

| Key highlights: |

🇯🇵 GDP (QoQ) (Q4) – Monday 07:50

🇩🇪 German CPI (MoM) (Jan) – Tuesday 15:00

🇳🇿 RBNZ Interest Rate Decision – Wednesday 09:00

🇬🇧 CPI (YoY) (Jan) – Wednesday 15:00

🇺🇸 Durable Goods Orders (MoM) (Dec) – Wednesday 21:00

🇺🇸 FOMC Meeting Minutes – Thursday 03:00

🇺🇸 Philadelphia Fed Manufacturing Index (Feb) – Thursday 21:30

🇺🇸 Initial Jobless Claims – Thursday 21:30

🇺🇸 Core PCE Price Index (MoM) (Dec) – Friday 21:30

🇺🇸 GDP (QoQ) (Q4) – Friday 21:30

🇺🇸 Core PCE Price Index (YoY) (Dec) – Friday 21:30

🇺🇸 S&P Global Manufacturing PMI (Feb) – Friday 22:45

🇺🇸 S&P Global Services PMI (Feb) – Friday 22:45

🇺🇸 New Home Sales (Dec) – Friday 23:00

Macro Analysis:

🇯🇵 Japan Growth Anchor (GDP QoQ, Q4) – Mon: Sets the early-week Asia tone. A stronger print supports JPY risk-on confidence; a weaker print can lean defensive and lift safe-haven flows.

🇩🇪 EUR Inflation Pulse (German CPI MoM, Jan) – Tue: Key EUR risk-tone driver for the week. A hotter print can firm EUR via rate expectations; a softer print does the opposite.

🇳🇿 RBNZ Policy Decision – Wed: The main NZD volatility point. Even without a surprise move, guidance and language can swing NZD pairs quickly (hawkish tilt supports NZD; dovish tilt pressures it).

🇬🇧 UK Inflation Signal (CPI YoY, Jan) – Wed: A rates-expectations mover for GBP. Upside inflation surprise tends to support GBP; downside can trigger repricing lower.

🇺🇸 U.S. Activity Pulse (Durable Goods Orders MoM, Dec) – Wed: A front-end growth check into the heavier U.S. block later in the week. Weakness can amplify growth worries; strength can support USD via relative yields.

🇺🇸 Fed Communication Anchor (FOMC Meeting Minutes) – Thu: The main USD volatility anchor this week. The catalyst is not “policy action” but how the minutes frame inflation progress, labour tightness, and the path for rates.

🇺🇸 U.S. Labour + Factory Stress Check (Initial Claims + Philly Fed) – Thu: A dual read on employment conditions and manufacturing momentum. Lower claims / stronger Philly tends to support USD and yields; deterioration can lean risk-off.

🇺🇸 U.S. Macro “Cluster” (Core PCE MoM/YoY + GDP QoQ, Q4) – Fri: The week’s biggest repricing window. Core PCE drives inflation expectations; GDP shapes the growth narrative—together they can reset rate-path pricing and USD direction.

🇺🇸 U.S. Activity Confirmation (S&P Global Manufacturing/Services PMI + New Home Sales) – Fri: Post-core data validation of momentum. Stronger prints support risk and USD through yields; weaker readings can fade any bullish repricing and revive slowdown concerns.

Speculative Outlook for USD Traders:

This is a Fed-minutes + late-week inflation/growth confirmation week, so positioning can reprice fast depending on rates expectations, yields, and Friday’s data cluster.

Check out full here: Followme Economic Calendar Tool

Follow Followme for the newest market updates

Peringatan: Pendapat yang disampaikan sepenuhnya merupakan milik penulis dan tidak mencerminkan posisi resmi Followme. Followme tidak bertanggung jawab atas keakuratan, kelengkapan, atau keandalan informasi yang disediakan, serta tidak bertanggung jawab atas tindakan apa pun yang diambil berdasarkan konten ini, kecuali dinyatakan secara tertulis.

- AKHIR -